How to get a startup business loan with no money is one of the most common questions first-time entrepreneurs ask — and the answer is yes, it is possible. You have the idea, you have the drive, but no revenue coming in yet. Here’s exactly where to look and how to prepare.”

Most traditional banks will turn you away. They want two years of business history, strong revenue, and solid credit. You have none of that yet. But that doesn’t mean you’re out of options. There are lenders, programs, and funding strategies built specifically for entrepreneurs in your exact situation.

This guide breaks down everything — the real loan options, the smart loans and funding strategies, how to improve your chances, and what to avoid.

Is It Really Possible to Fund a Business From Zero?

Yes — but let’s be honest about what “no money” actually means to a lender.

When you apply for a startup loan without revenue, a lender has no historical cash flow to assess. That makes you a higher-risk borrower. To compensate, lenders will look at other signals:

- Your personal credit score

- Your business plan and financial projections

- Any collateral you can offer (equipment, property, etc.)

- A personal guarantee (you personally agree to repay if the business can’t)

- The strength of your idea and market opportunity

The bottom line: you cannot replace revenue with nothing. But you can replace revenue with a strong credit profile, a compelling business plan, and the right type of lender.

Why Banks Usually Say No to Startups

Before diving into solutions, it helps to understand why traditional banks reject most startup loan applications.

Banks reject startups because of four core reasons:

- No Revenue — Lenders use consistent income to predict repayment ability. Without it, there’s no data to support approval.

- No Collateral — Banks want assets they can seize if you default. Most new founders haven’t accumulated business assets yet.

- Limited Credit History — Your business has no credit score because it hasn’t borrowed before. A thin credit profile raises lender risk.

- Statistical Risk — Banks know that approximately 21.5% of businesses fail in their first year. Without revenue, that risk increases in their eyes.

Understanding these objections is the first step. The strategies in this guide are specifically designed to address each one.

8 Real Funding Options for New Entrepreneurs

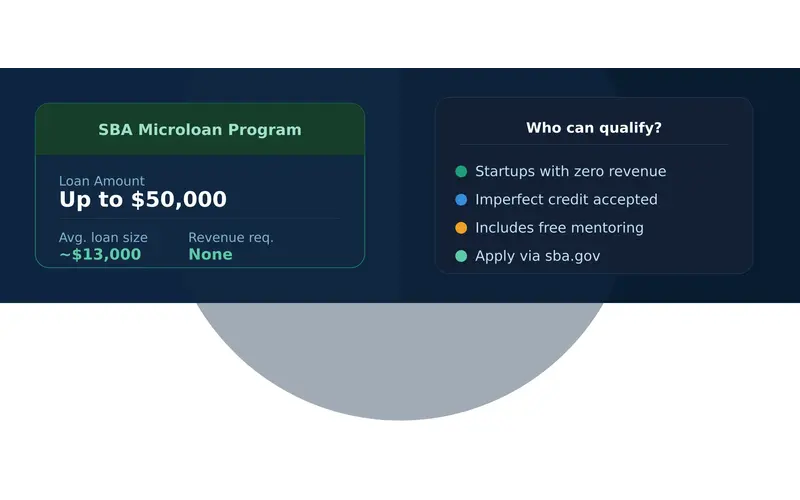

1. SBA Microloans — Best for Startups Under $50,000

The U.S. Small Business Administration (SBA) Microloan program is one of the best-kept secrets in startup funding. It offers loans of up to $50,000 specifically designed for small businesses and startups that struggle to qualify for traditional financing.

Key facts:

- Loan amounts: Up to $50,000

- Average loan size: Around $13,000

- Delivered through nonprofit community lenders and CDFIs (Community Development Financial Institutions)

- Often includes business mentoring and training alongside the funding

- More flexible qualification requirements than bank loans

Who qualifies: Microloans are available to startups with limited or no revenue. Lenders typically evaluate your credit score, business plan, and potential — not just current cash flow. Even borrowers with imperfect credit may qualify.

How to apply: Visit the SBA website (sba.gov) and search for SBA Microloan intermediaries in your area. Each intermediary sets its own specific requirements, so contact several in your region.

Pro Tip: Pair your microloan application with a solid business plan and any free mentoring you can access through SCORE or your local Small Business Development Center (SBDC). Lenders respond well to applicants who demonstrate preparation.

2. Equipment Financing — Best if You Need Machinery or Tools

If your startup needs equipment to operate — machinery, vehicles, computers, restaurant equipment, medical devices — equipment financing is one of the most accessible options for businesses with no revenue.

Why it works for startups: The equipment itself acts as collateral for the loan. This dramatically reduces the lender’s risk, which means they care far less about your revenue history and far more about the value of the asset being financed.

Key facts:

- Some equipment lenders have no minimum revenue requirement

- No minimum time in business required by many providers

- Can finance up to 100% of the equipment cost

- Loan terms are typically tied to the useful life of the equipment

What lenders assess instead of revenue: Your personal credit score, the value and utility of the equipment, and how well the equipment fits your business plan.

Pro Tip: When applying, show the lender how the equipment directly generates income for your business. A food truck that generates direct sales or a CNC machine that fulfills contracts is easier to finance than general office furniture.

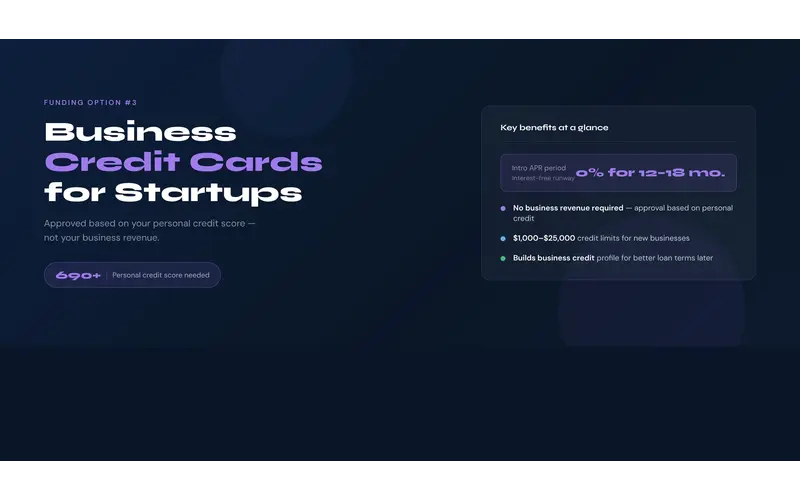

3. Business Credit Cards — Best for Day-to-Day Startup Expenses

A business credit card is often overlooked as a funding tool, but it is one of the most accessible options for new founders with no business revenue.

Why it works: Most business credit card issuers base approval primarily on your personal credit score, not your business revenue. If you have a personal credit score of 690 or above, you have a strong chance of qualifying.

Key facts:

- Revolving credit: spend, repay, and reuse

- Many cards offer 0% APR introductory periods (12–18 months), giving you interest-free runway

- Builds your business credit profile, which unlocks better loan terms later

- Credit limits typically range from $1,000 to $25,000 for new businesses

Best used for: Inventory, software subscriptions, marketing spend, and operating costs — not large capital investments.

Pro Tip: Pay your balance in full every month. Your payment history is the single biggest factor in building business credit. A strong business credit profile in year one opens significantly better loan options in year two.

4. Personal Loans for Business — Best When Business Credit Isn’t Established Yet

A personal loan used for business purposes is a legitimate and widely-used funding strategy for early-stage startups. Because the loan is based on your personal financial profile, your business’s lack of revenue is irrelevant.

Key facts:

- Loan amounts: typically $1,000–$100,000

- APR range: roughly 6–36% depending on your personal credit

- Approval based entirely on personal credit score, income, and debt-to-income ratio

- Funds can be used for any business purpose

Risks to understand: With a personal loan, you are personally liable for repayment regardless of what happens to your business. If the business fails, the loan obligation does not disappear. Only borrow what you can genuinely afford to repay from personal income if needed.

Pro Tip: If your personal credit score is below 620, work on improving it before applying. Even a few months of on-time payments on existing debts can meaningfully improve your score and lower your interest rate.

5. Crowdfunding — Best for Consumer Products and Creative Ideas

Crowdfunding platforms allow you to raise startup capital from the public — without taking on debt or giving up equity (depending on the model you choose).

Types of crowdfunding:

| Type | How It Works | Best For |

| Reward-based | Backers receive a product or perk | Consumer products, creative projects |

| Equity-based | Backers receive a small ownership stake | Tech startups, scalable businesses |

| Debt-based | Multiple investors lend money, you repay with interest | Revenue-generating businesses |

| Donation-based | Backers donate with no financial return | Social enterprises, nonprofits |

Popular platforms: Kickstarter (rewards), Indiegogo (rewards/equity), Wefunder (equity), Republic (equity)

What makes a campaign succeed: The platforms themselves don’t provide funding — your audience does. Campaigns that reach their goals typically have strong visual storytelling, a clear product or mission, a realistic funding target, and an existing audience or community to launch to.

Pro Tip: Build your email list and social media following before you launch your campaign. Campaigns that hit 30% of their goal within the first 48 hours have dramatically higher success rates.

6. Grants — Best Free Money (No Repayment Required)

Business grants are funds awarded to qualifying businesses that never need to be repaid. For the right entrepreneur, a grant is the most valuable form of startup funding available.

Types of grants worth exploring:

- Federal grants: Grants.gov lists thousands of federal funding opportunities. SBIR (Small Business Innovation Research) grants are particularly valuable for technology and science-based startups.

- State and local grants: Most states offer economic development grants for small businesses, especially in underserved areas.

- Minority and women-owned business grants: Organizations like the Amber Grant (women-owned), IFundWomen, and the National Minority Supplier Development Council offer targeted funding.

- Corporate grants: Companies like FedEx, Visa, and Amazon run annual small business grant programs with cash awards up to $50,000.

The honest reality about grants:

Grants are competitive and require significant time to research and apply for. Most are industry or demographic specific. Treat grant applications as a parallel strategy alongside other funding, not your only plan.

Pro Tip: Start with your state’s Small Business Development Center (SBDC). They maintain updated lists of available local grants and can help you write a stronger application for free.

7. Friends, Family & Angel Investors — Best for Early Validation

For many startups, the first funding comes from the people closest to them — or from individual investors who believe in the idea before the market does.

Friends and family funding:

- Typically informal, low or no interest

- Based on personal trust rather than financial metrics

- Risk: mixing money and personal relationships. Always document the terms in writing, even informally.

Angel investors: Angel investors are high-net-worth individuals who invest their personal capital in early-stage businesses in exchange for equity (ownership) or convertible debt.

- Average angel investment: $25,000–$500,000

- They invest at the idea or early-traction stage

- They often provide mentorship and introductions alongside capital

- Find angels through AngelList, local startup ecosystems, and pitch competitions

What angels look for: Unlike banks, angels are evaluating the size of the market opportunity, the quality of the founder, and the uniqueness of the solution — not current revenue.

Pro Tip: Before approaching investors, be able to answer three questions clearly: What problem are you solving? Why is now the right time? Why are you the right person to solve it?

8. CDFIs and Nonprofit Lenders — Best for Underserved Entrepreneurs

Community Development Financial Institutions (CDFIs) are mission-driven lenders that specifically serve entrepreneurs who can’t access traditional bank financing. They exist to fund businesses in underserved communities, lower-income areas, and minority-owned startups.

Key advantages over banks:

- Lower minimum credit score requirements (some as low as 580–620)

- More flexible underwriting — they consider your story and potential, not just numbers

- Often offer financial coaching and business training alongside the loan

- Loan amounts: typically $500–$250,000

Notable CDFI lenders:

- Accion Opportunity Fund — minimum credit score around 620, may work lower case-by-case

- Kiva — 0% interest loans up to $15,000, funded by the community, no minimum credit score

- Grameen America — microloans for women entrepreneurs, no credit score requirement

Pro Tip: Kiva is particularly worth exploring if your credit is poor. Loans are crowd-funded, interest-free, and Kiva charges no fees. The trade-off is that you need to fundraise your loan through your personal network first.

For a complete breakdown of managing startup finances from day one, read our step-by-step financial guide for new business owners.

Startup Business Loans With No Revenue and Bad Credit — Is It Possible?

Yes, but your options narrow significantly and costs go up. Here is what’s realistic:

Options that work with bad credit:

- Kiva microloans — no minimum credit score

- Secured loans — where collateral offsets credit risk

- CDFIs — case-by-case assessment, not purely score-based

- Merchant cash advances — based on future sales projections, not credit history (but extremely expensive — avoid unless desperate)

- Invoice financing — based on client creditworthiness, not yours

What “bad credit” actually means to lenders:

- Below 580: Very limited options, expect high rates and strict terms

- 580–620: Some CDFI and alternative lenders will work with you

- 620–680: More options open up, including some SBA microloan intermediaries

- 680+: You qualify for most startup funding options

How to improve your credit before applying:

- Check your credit report for errors (dispute anything inaccurate through Equifax, Experian, or TransUnion)

- Pay down existing credit card balances to below 30% of your limit

- Make every payment on time for 3–6 months before applying

- Avoid opening multiple new credit accounts before applying

Even three months of disciplined credit management can meaningfully move your score. If you’re at 560 today, getting to 620 unlocks significantly better options.

How to Get a Startup Business Loan With No Money: Step-by-Step Application Guide

Follow these steps to give yourself the best possible chance of approval.

Step 1: Know Your Numbers Before You Apply

Before approaching any lender, understand your financial position clearly:

- What is your personal credit score? (Check free via AnnualCreditReport.com or Credit Karma)

- What assets do you own that could serve as collateral?

- What is your personal debt-to-income ratio?

- How much do you actually need — and how will you use it?

Lenders will ask all of these questions. Being prepared signals professionalism and reduces their perceived risk.

Step 2: Write a Detailed Business Plan

A strong business plan shows a lender you have thought rigorously about risk. Use our free business plan template to structure yours before applying.

Your business plan must include:

- Executive summary — what your business does and why it will succeed

- Market analysis — the size of your market and evidence of demand

- Competitive analysis — what exists, why you’re different

- Revenue model — exactly how you will make money

- Financial projections — realistic 12–24 month forecasts (revenue, expenses, cash flow)

- Loan use of funds — a specific breakdown of how every dollar will be spent

- Repayment plan — how you will repay the loan even if growth is slower than projected

A strong business plan shows a lender you have thought rigorously about risk. It doesn’t guarantee approval, but the absence of one almost guarantees rejection.

Step 3: Choose the Right Loan Type for Your Situation

Match your loan type to your specific situation:

| Your Situation | Best Option |

| Need under $50K, flexible terms | SBA Microloan or CDFI |

| Need equipment | Equipment financing |

| Have bad credit | Kiva, CDFIs, secured loans |

| Have a product idea | Crowdfunding |

| Have a strong personal credit score | Personal loan or business credit card |

| Have investors interested | Angel investment |

Don’t apply to the wrong type of lender. Rejections hurt your credit and waste time.

Step 4: Prepare Your Documentation

Gather these documents before applying:

- Government-issued ID

- Social Security Number (for personal credit check)

- Business registration documents (LLC, EIN, etc.)

- Business plan with financial projections

- Personal tax returns (last 1–2 years)

- Personal bank statements (last 3–6 months)

- List of any business or personal assets

The more organised your documentation, the faster and smoother your application process.

Step 5: Apply to Multiple Lenders

Don’t put all your eggs in one basket. Apply to 3–5 lenders simultaneously. Different lenders have wildly different risk appetites, and rejection from one does not predict rejection from another.

When comparing loan offers, evaluate:

- Annual Percentage Rate (APR) — not just the interest rate

- Total repayment cost (not just monthly payment)

- Repayment term length

- Prepayment penalties

- Personal guarantee requirements

Step 6: Negotiate and Review Before Signing

Never accept the first offer without scrutiny. Key things to watch for:

- Interest rates significantly higher than competitors — a red flag for predatory lending

- Fees exceeding 5% of the loan value — ask for a full fee breakdown

- Blank signature boxes — never sign an incomplete document

- Pressure tactics — legitimate lenders give you time to review

If anything feels unclear, consult a financial advisor or your local SBDC counsellor before signing. This service is typically free.

5 Ways to Strengthen Your Application Right Now

Even before applying, these steps materially improve your approval odds:

- Offer Collateral

Any valuable asset — equipment, a vehicle, savings account, real estate — reduces lender risk. Secured loans are significantly easier to get than unsecured ones when you have no revenue.

- Add a Co-Signer

A co-signer with excellent credit and strong personal assets agrees to repay the loan if you cannot. This can be the difference between approval and rejection for early-stage founders.

- Build Your Business Credit Immediately

Open a business bank account and business credit card the moment you register your business. Use them regularly and pay on time. Every month of positive credit history counts.

- Get Your Business Legally Registered

Register your LLC or corporation, get your EIN (Employer Identification Number), open a business bank account, and separate your personal and business finances completely. Lenders take unregistered businesses far less seriously.

- Seek Free Mentoring First SCORE (score.org) offers free mentoring from experienced business executives. Small Business Development Centers (SBDCs) are funded by the SBA and offer free consulting. Both services help you strengthen your business plan, identify the right funding options, and prepare for lender conversations. Most approved startup borrowers have used at least one of these resources.

What to Avoid: Red Flags and Costly Mistakes

Avoid merchant cash advances (MCAs) unless absolutely necessary

MCAs advance you money based on future sales and collect repayment via a daily percentage of revenue. They are fast and easy to get — but factor rates can translate to effective APRs of 40–150%. They are legal but extremely expensive, and can trap cash-strapped startups in a cycle of debt.

Avoid predatory lenders

Signs of a predatory lender: guaranteed approval regardless of credit, fees not disclosed upfront, pressure to sign quickly, requests to falsify information, or rates dramatically higher than the market average.

Don’t borrow more than you need

It’s tempting to take as much as you can get. But every dollar borrowed is a dollar that must be repaid with interest. Borrow specifically for what your business plan requires, not optimistically.

Don’t confuse funding sources

Equity investment (angel, VC) means giving up ownership. Debt (loans) means repaying with interest. Grants mean free money. Know which you’re pursuing and what the trade-offs are before committing.

Final Thoughts

Getting a startup business loan with no money is genuinely challenging — but it is not impossible.

The entrepreneurs who succeed do three things differently from those who don’t:

- They match their funding application to the right type of lender for their specific situation

- They invest time in a serious, detailed business plan rather than applying empty-handed

- They use every free resource available — SCORE mentors, SBDCs, grant programs — before spending a dollar

Start with your personal credit score and a clear business plan. Identify which option from this guide fits your current position. Then act — because the only startup that definitely never gets funded is the one that never applies.

Frequently Asked Questions

Can I get a startup business loan with no money and no credit?

Yes, but options are extremely limited. Kiva offers 0% interest community-funded loans with no minimum credit score. Some CDFIs also assess applicants holistically rather than by score alone. Expect lower loan amounts and a longer approval process.

What credit score do I need for a startup business loan?

It depends on the lender. Traditional banks typically want 680+. SBA microloan intermediaries may work with scores as low as 620. CDFIs and Kiva may work with scores below 600 on a case-by-case basis.

How much can I borrow as a startup with no revenue?

Microloans: up to $50,000. Equipment financing: up to 100% of equipment cost. Personal loans: typically $1,000–$100,000. Crowdfunding: no fixed limit (depends on your campaign). The right amount is whatever your verified business plan demonstrates you need and can repay.

Do SBA loans require revenue?

Standard SBA 7(a) loans typically require at least some revenue history. However, SBA Microloans (up to $50,000) are specifically designed for startups and pre-revenue businesses, and requirements vary by intermediary lender.

What is the easiest loan to get for a startup?

Kiva microloans and business credit cards are generally the most accessible for founders with limited credit and no revenue. Equipment financing is also accessible if you need to purchase specific assets.

Can I get a startup loan if I have bad credit?

Yes — through CDFIs, Kiva, secured loans (backed by collateral), and certain nonprofit lenders. You should also spend 3–6 months actively improving your credit score in parallel with exploring these options.

How long does it take to get a startup business loan?

It varies significantly: business credit cards (1–7 days), online personal loans (1–3 days), equipment financing (1–2 weeks), SBA microloans (2–4 weeks), grants (weeks to months).